PPF Loan: Get a Low-Interest Emergency Loan Without a Personal Loan – Eligibility, Rules & Benefits

Need emergency funds? Learn how to get a low-interest loan against your PPF account instead of taking an expensive personal loan. Check eligibility, loan limits, repayment rules, and key benefits.

RJ Kesari News Desk: Unexpected financial emergencies can arise at any time, whether it's a medical expense, home repair, or any urgent need for cash. In such situations, many people immediately think of personal loans or credit cards, but these options often come with high interest rates and long repayment burdens.

If you have a Public Provident Fund (PPF) account, there's a much smarter and cheaper option available. A loan against your PPF account allows you to access funds at a significantly lower interest rate without lengthy paperwork or the need for collateral.

Here's everything you need to know.

What Is a Loan Against a PPF Account?

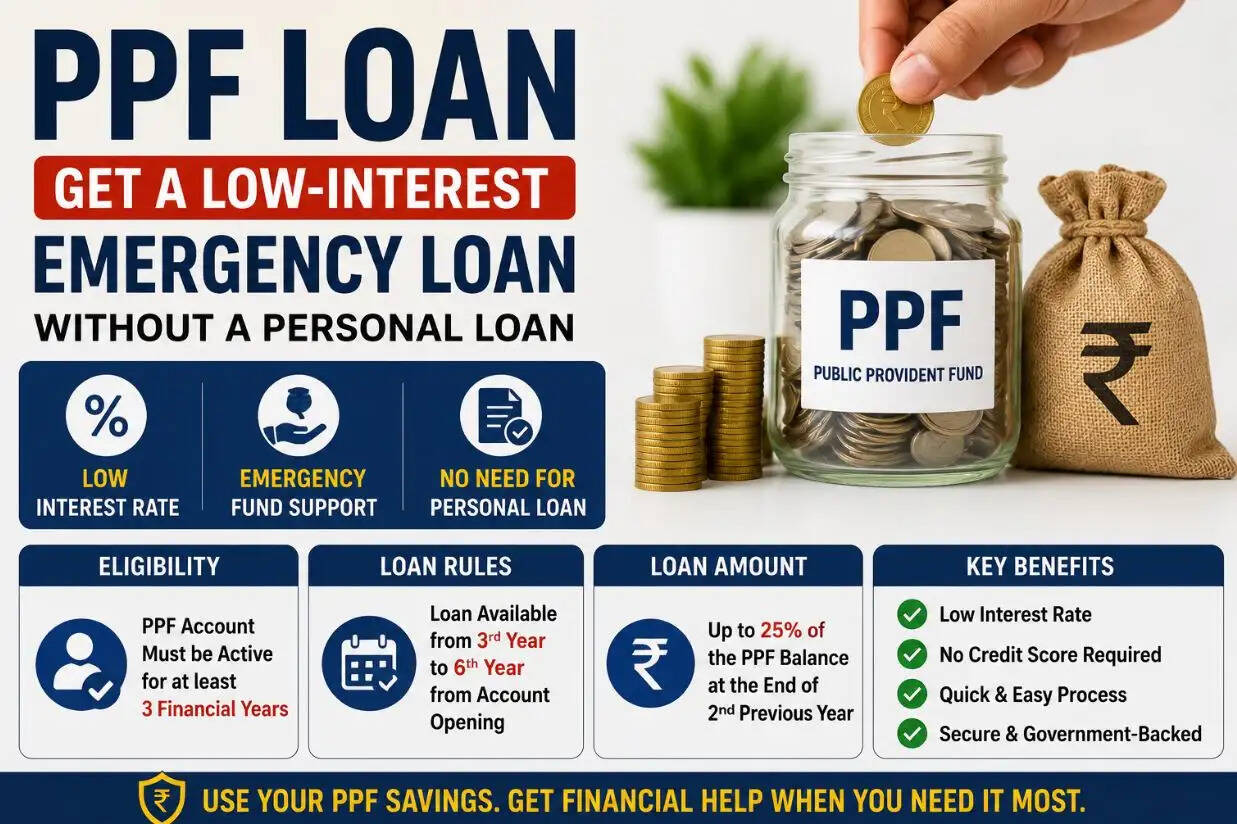

A PPF loan is a facility that allows account holders to borrow money against the balance available in their Public Provident Fund account.

Since the loan is backed by your own savings, banks and post offices offer it at much lower interest rates than unsecured loans like personal loans.

This makes it one of the most affordable borrowing options during financial emergencies.

When Can You Apply for a PPF Loan?

Although a PPF account has a 15-year maturity period, you cannot apply for a loan throughout the entire tenure.

According to PPF rules, the loan facility is available:

- From the beginning of the third financial year after opening the account.

- Until the end of the sixth financial year.

Example

If your PPF account was opened during FY 2023-24, you can apply for a loan between:

- FY 2025-26 and

- FY 2028-29

After this period, the loan facility ends, and account holders become eligible for partial withdrawals instead.

How Much Loan Can You Get?

The loan amount is not calculated based on your current balance alone.

Under PPF rules, you can borrow up to 25% of the balance available at the end of the financial year immediately preceding the year in which you apply.

Because of this calculation method, the sanctioned amount may be lower than your current account balance.

Why a PPF Loan Is Better Than a Personal Loan

Choosing a loan against your PPF account offers several financial advantages.

1. Lower Interest Rates

Since you're borrowing against your own investment, the interest rate remains much lower than that of personal loans or credit cards.

2. Minimal Documentation

Unlike traditional loans, there is no need for extensive paperwork, guarantors, or complicated verification.

3. No Credit Score Worries

Approval is linked to your PPF account balance rather than your credit history, making the process faster and hassle-free.

Repayment Rules You Should Know

A PPF loan is designed as a short-term financial solution.

- The principal amount must be repaid within 36 months from the first day of the month following loan approval.

- Interest is payable only after the principal has been fully repaid.

- Delayed repayment may attract additional interest or penalties.

- You cannot apply for another PPF loan until the previous one has been completely repaid.

Who Should Consider a PPF Loan?

A loan against your PPF account can be an excellent choice if you need funds for:

- Medical emergencies

- Education expenses

- Home repairs or renovation

- Family emergencies

- Temporary cash flow shortages

Instead of paying high interest on unsecured loans, using your own savings can significantly reduce your borrowing cost.